Money Management is the key to paying off debt. This guide will help you create a money management strategy to pay down debt and increase your net worth

Money Management – In the Beginning

I’ve always tracked my spending using software from Microsoft Money to Quicken 2017. These applications made it very easy to import and categorize my transactions. As well to see how much money I had left each month.

Although I was tracking my spending. I would always have an unexpected expense pop up. Expenses such as an auto repair or an irregular expense that I didn’t prepare for. I knew I needed a solution. A strategy that would reduce the unexpectedness.

The Jars System

I found that strategy when I stumbled upon the book Secrets of the Millionaire Mind by T. Harv Ecker. In his book Harv introduces his readers to the 6 Jars money management system. The idea of the system is to separate your income into 6 different accounts. Each of the 6 different accounts serve a specific purpose.

The jars themselves aren’t actually that important. What’s more important is the money management system behind them. I manage my system from a set of bank accounts. One of the benefits of using this system is that it’s very flexible. You can adjust the percentages that work for your current situation. I have also adjusted the system by adding extra jars.

First, I will go over the original system and then I will show you how I use the system to suit my needs.

The Original System

Financial Freedom Account (FFA – 10%): This is your golden goose. This jar is your ticket to financial freedom. The money you put into this jar is for investments and building your passive income streams. You never spend this money. The only time you would spend this money is once you become financially free. Even then you would only spend the returns on your investment. Never spend the principal.

Long-term saving for spending Account (LTS – 10%): Money in this jar is for bigger purchases. Use the money for vacations, a plasma TV, contingency fund, or your children’s education. A small monthly contribution can go a long way. You may have more than one LTS jar. If you have more than one LTS, divide the 10% between the jars according to your priorities.

Education Account (EDU – 10%): You can use the EDU funds for your self-education. Examples include books, seminars and events. Everyone needs to learn, especially in this fast changing world. Grow your comfort zone through learning and risking. Challenge yourself! There are only two things to remember in this world, if you are not growing, you are dying!

Give Account (GIV – 5%): Money in this jar is for giving away. Use the money for family and friends on birthdays, special occasions and holidays. You can also give away your time as opposed to giving away money. You could house sit for a neighbor, take a friend’s dog for a walk or volunteer in your community or favorite charity.

Necessity Account (NEC – 55%): This account is for managing your everyday expenses and bills. This includes your rent, mortgage, utilities, bills, food, or clothes. It includes anything that you need to live, the necessities.

Play Account (PLY – 10%): You spend this money every month to pamper yourself. The key is to BLOW this Play money away every month so that you will feel good about having money and spending it! You should feel guilt-free when you spend this money every single month. You could buy an expensive bottle of wine at dinner, get a massage or go on a weekend getaway.

My Modified System

My system includes all the above mentioned jars and adds 3 more. The 3 jars are:

Short Term Savings: This jar is for saving for short term spending. Yearly expenses, birthdays and holiday gifts are all saved for in this account.

Debt Paydown: This jar is for paying down my debt. One of the last things I account for is extra money to speed up my debt paydown.

Investing: This jar is like the financial freedom jar except that I use this jar while paying down my debt. I use this jar to fund my investment accounts.

My Custom Allocations

Along with custom categories, I also have custom percentage allocations. This is the reason I like this system so much. It is completely customize-able.

Necessity Account (NEC – 95%):

Financial Freedom Account (FFA – 2%):

Long-term saving for spending Account (LTS – 1.25%):

Education Account (EDU – .3%):

Give Account (GIV – 0%):

Play Account (PLY – 1.35%):

Short Term Savings: (STS – 1.5%)

Debt Paydown: (DP – 90% of remaining funds)

Investing: (INV – 10% of remaining fund)

On to the Budget

What do you think about when you hear the word budget? To most, the word budget is not a nice word, equated to restriction and a lack of fun and joy. In reality, a budget is a guide for your money.

A budget allows you to no longer stress over the uncertainty of not having a plan for your money. Have you ever taken money out of the ATM, only to wonder a few days later, where it all went? A budget eliminates that wondering and replaces it with knowledge.

My system uses 2 budgets one that utilizes the zero-based budget concept and one that does not.

The Zero-Based Budget

The concept of a zero-based budget is simple. Each month, your goal is to plan how you’re going to “spend” all your income. Your goal is to get your budget to “zero”. An equation to represent this approach would look like this:

Income – Expenses = Zero

You have 2 budgets? Are you crazy?

Yes I may be crazy, but hear me out. I found that based on my personality I would need a budget that was static. As well as one that could change throughout the month. By having 2 budgets I was able to achieve two things.

- I was able to plan for the month ahead, before the first check of the month.

- I was able to compare the static budget with the flexible budget to see if any changes had occurred. Was there a bill I missed during the initial budgeting? Am I putting enough away for unexpected expenses? One budget could answer these questions over time. 2 budgets can answer these and other questions much more quickly.

So how do I get my budget on?

I’m glad you asked. My first step is to set up my monthly budget using my fixed budget.

-

First, I list all my income sources for the month.

This includes paychecks, small-business income, side jobs, residual income and so on. I use my fixed budget for this.

-

Then I pay myself first.

By listing all my saving goals, I make sure that get funded before I pay my expenses. This means I have no excuse to save.

-

Next, I list every expense I have for the month.

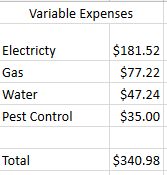

Rent, food, cable, phones and everything between gets added to the list. I separate my expenses between fixed, variable and irregular.

Fixed: For fixed expenses, I enter them as they are.

Examples of fixed expenses: rent, loan payments.

Variable: For variable expenses I take the average of 3 – 12 months of the expense.

Examples of variable expenses: utilities.

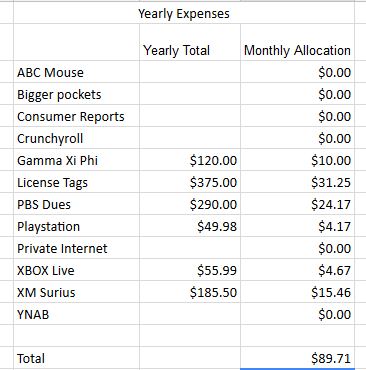

Irregular: I take the total amount of the expense and divide it by the frequency that it is due.

Example, yearly expenses I divide by 12, quarterly expenses, I divide by 4.

-

Subtract your income from you expenses.

Finally I subtract my income from my expenses, savings and giving. Whatever left, I split 90/10 between debt paydown and investing.

The Monthly Workflow

Day One

Create your budget(s)

Then set up your accounts: Make sure that you have your accounts are setup before your income starts to come in.

Pay Day

I update my working budget to give all my income a place to go.

Twice a Month

I’ve chosen the 3rd and the 17th for my days.

- First, transfers go made from my income account to my other accounts based on the amounts I entered in my budget.

- Then, any money that needs to be in the expenses account to cover bills I transfer it now

- Finally, bills that are due between the due date and the next date get paid, if they have not been set up for auto pay.

Every Month

I take any funds left over for the month and split them as followed:

90% Debt Paydown

10% Investment Capital

Every Other Month

I take the funds from the debt paydown category and put it towards which ever debt I am working on at the moment.

Every Quarter

I take half of the funds from the financial freedom account. I have debt so I take 90% of that for debt paydown, with the remaining funds going to my play account. If I had no debt, then I would celebrate with that money.

Let’s go to work

Now that we have a game plan, the only thing left to do is to put that plan into action.